Understanding Hidden Costs: What Your Home Loan Really Entails

When considering a home loan, many potential homeowners focus primarily on the interest rate and monthly payments, but it's crucial to understand the hidden costs that can significantly affect your financial commitment. One major hidden cost is closing costs, which can range from 2% to 5% of the loan amount. These include appraisal fees, title insurance, and attorney fees, all of which can add thousands to your initial outlay. Additionally, you might face ongoing costs such as property taxes and homeowner's insurance that may not be factored into your loan calculations.

Another often-overlooked consideration is maintenance costs. Owning a home comes with the responsibility of upkeep, which can amount to about 1% of your home's value annually. For a $300,000 home, that translates to approximately $3,000 each year. It's also wise to set aside funds for emergency repairs, which could otherwise be a shock to your budget. By being informed about these potential expenses, you can choose a home loan that aligns better with your financial capabilities and avoid unexpected financial strain down the line. For more insights, check out this HUD resource on home maintenance.

Is Your Home Loan a Financial Trap? Key Questions to Ask

When considering a home loan, it's essential to ask if the terms are truly beneficial or if you're stepping into a financial trap. Begin by evaluating the interest rates offered. Are they fixed or variable? A fixed-rate mortgage offers predictable payments, while a variable-rate mortgage can fluctuate and increase your financial burden over time. In addition to interest rates, examine the loan term and whether the monthly payments fit comfortably within your budget. Ask yourself: What are the penalties for early repayment? Understanding the full scope of your home loan can prevent financial pitfalls down the road.

Another critical question revolves around hidden fees. Ensure you review the loan disclosure documents thoroughly. Look for additional costs such as closing costs, origination fees, and other miscellaneous charges that could trap you in an unfavorable financial situation. Finally, assess your future financial plans: Will this loan align with your long-term goals? A comprehensive understanding of these elements can help you avoid falling into a financial trap and provide peace of mind as you navigate homeownership.

Navigating the Mortgage Maze: Tips for First-Time Homebuyers

Buying a home for the first time can feel overwhelming, especially when it comes to understanding mortgages. To simplify the process, start by familiarizing yourself with key terms such as principal, interest, and amortization. Many potential buyers overlook the importance of shopping around for the best mortgage rates. Consider using online mortgage comparison tools to evaluate different lenders and their offerings. It's also beneficial to get pre-approved for a mortgage, as this will give you a clearer picture of your budget and show sellers that you're a serious buyer. For more detailed information, visit Consumer Financial Protection Bureau.

Once you have a better idea of your financing options, understanding the different types of mortgages available can save you a lot of time and frustration. Here are a few options to consider:

- Fixed-Rate Mortgages: These loans have a constant interest rate and monthly payments that never change.

- Adjustable-Rate Mortgages (ARMs): These may start with lower rates but can adjust higher after a set period.

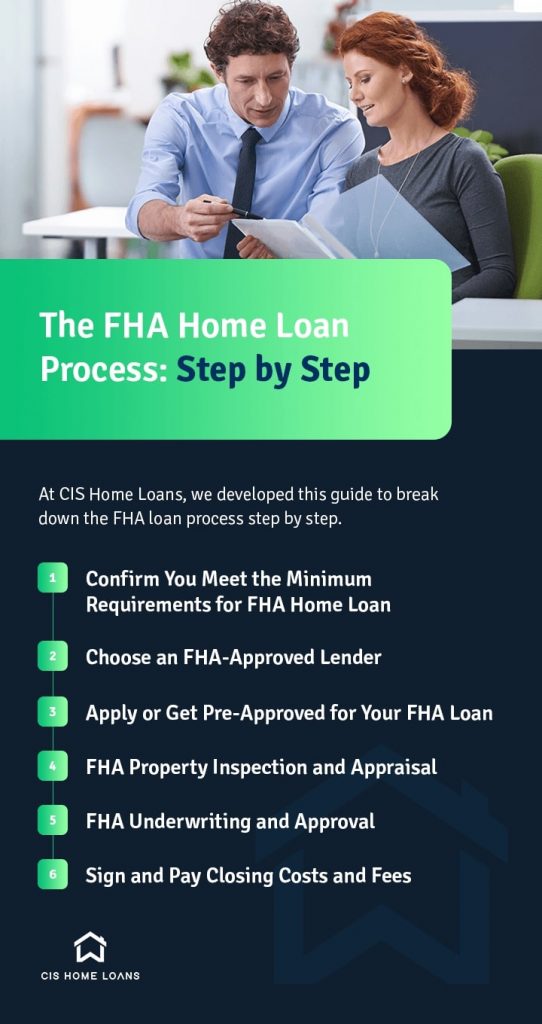

- FHA Loans: Government-backed loans that can be easier to qualify for, especially for first-time buyers.

Be sure to evaluate how each type aligns with your financial goals and long-term plans. For expert advice on choosing the right mortgage, check out National Association of Home Builders.